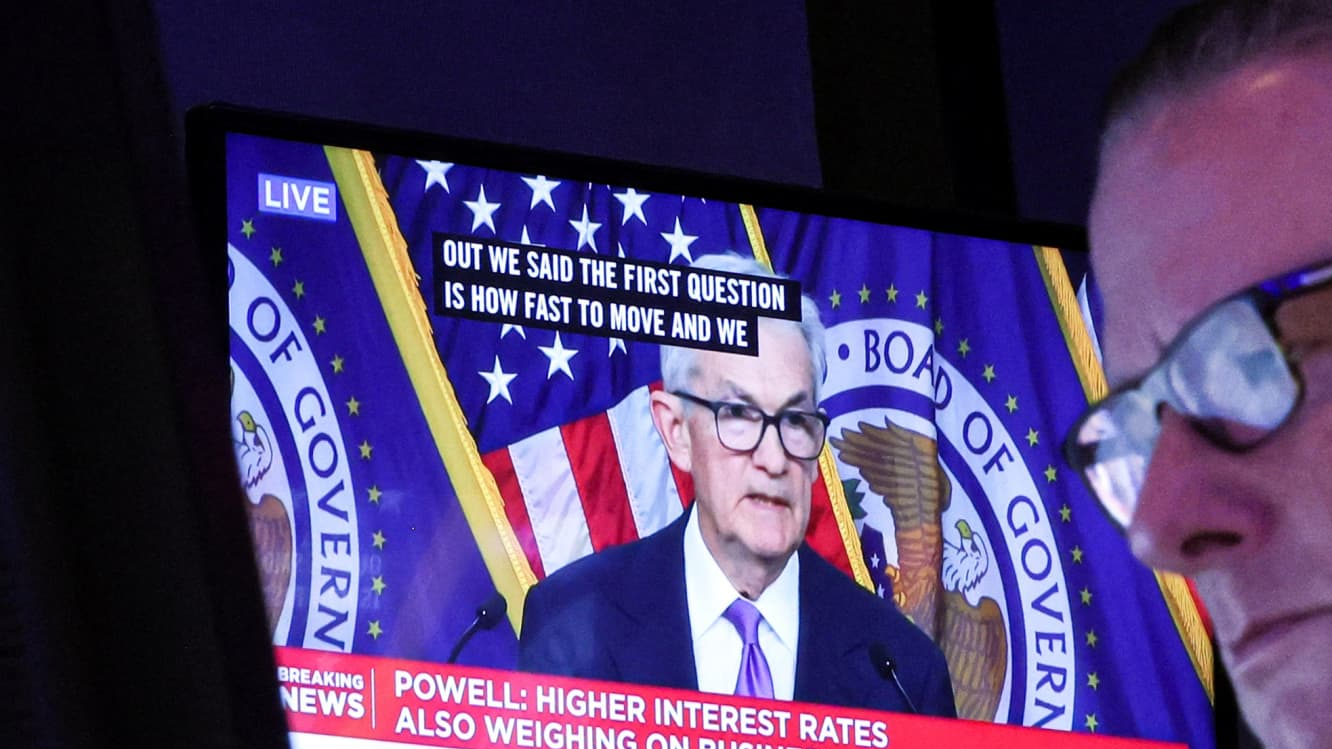

The Federal Reserve is expected to lower interest rates by another quarter point on Dec. 18 at the end of its two-day meeting. That would mark the third rate cut in a row — all together shaving a full percentage point off the federal funds rate since September.

So far, the central bank has moved slowly as they recalibrate policy after swiftly hiking rates when inflation hit a 40-year high.

“This could be the last cut for a while,” said Jacob Channel, senior economic analyst at LendingTree.

The Fed might choose to take “a wait-and-see approach” because there is some uncertainty around President-elect Donald Trump’s fiscal policy when he begins his second term, Channel said.

In the meantime, high interest rates have affected all sorts of consumer borrowing costs, from auto loans to credit cards.

More from Personal Finance:

Economy faces ‘some potential storms’ in 2025

Economists have ‘really had it wrong’ about recession

Trump tariffs would likely have a cost for consumers

The federal funds rate, which the U.S. central bank sets, is the rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and savings rates consumers see every day.

A December cut could lower the Fed’s overnight borrowing rate by a quarter percentage point, or 25 basis points, to a range of between 4.25% and 4.50% from its current range of between 4.50% and 4.75%.

That “will exert some margin of easing of financial pressure,” said Brett House, economics professor at Columbia Business School, but not across the board.

“Some of the most important interest rates that people face don’t benchmark off the Fed rate,” he said.

From credit cards to car loans to mortgages, here’s a breakdown of how it works:

Since most credit cards have a variable rate, there’s a direct connection to the Fed’s benchmark. In the wake of the rate hike cycle, the average credit card rate rose from 16.34% in March 2022 to 20.25% today, according to Bankrate — near an all-time high.

Even though the central bank started cutting interest rates in September, the average credit card interest rate has barely budged. Card issuers are often slower to respond to Fed decreases than to increases, said Greg McBride, Bankrate’s chief financial analyst.

“The rate will go a step lower but with a lag up to three months,” McBride said.

A better move for those with credit card debt is to switch to a 0% balance transfer credit card and aggressively pay down the balance, he said.

“Interest rates are not going to fall fast enough to do the heavy lifting for debt-burdened consumers,” he said.

Because 15- and 30-year mortgage rates are fixed and mostly tied to Treasury yields and the economy, they are not falling in step with Fed policy. And since most people have fixed-rate mortgages, their rate won’t change unless they refinance or sell their current home and buy another property.

As of the week ending Dec. 6, the average rate for a 30-year, fixed-rate mortgage is 6.67%, according to the Mortgage Bankers Association.

Those rates are down somewhat from the previous month, but well above the 2024 low of 6.08% in late September.

“Going forward, mortgage rates will likely continue to fluctuate on a week-to-week basis and it’s impossible to say for certain where they’ll end up,” Channel said.

Auto loans are fixed. However, payments have been getting bigger because car prices are rising and that has resulted in less-affordable monthly payments.

The average rate on a five-year new car loan is now around 7.59%, according to Bankrate.

While anyone planning to finance a new car could benefit from lower rates to come, the Fed’s next move will not have any material effect on what you get, said Bankrate’s McBride. “Sticker prices are high and the amounts being financed by borrowers are very, very high,” he said — around $40,000, on average.

“Even at very low rates, that is a budget-busting monthly payment,” he said.

Federal student loan rates are also fixed, so most borrowers won’t be immediately affected by a rate cut. However, if you have a private loan, those loans may be fixed or have a variable rate tied to the Treasury bill or other rates, which means as the Fed cuts rates, the rates on private student loans will come down as well.

Eventually, borrowers with existing variable-rate private student loans may also be able to refinance into a less-expensive fixed-rate loan, according to higher education expert Mark Kantrowitz.

However, refinancing a federal loan into a private student loan will forgo the safety nets that come with federal loans, he said, “such as deferments, forbearances, income-driven repayment and loan forgiveness and discharge options.”

Additionally, extending the term of the loan means you ultimately will pay more interest on the balance.

While the central bank has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate.

As a result of the Fed’s string of rate hikes in recent years, top-yielding online savings accounts have offered the best returns in decades and still pay nearly 5%, according to McBride.

“This is still a good time to be a saver and a good time for cash,” he said. “The most competitive offers are still well ahead of inflation and that’s likely to persist.”